How to Create a Personal Budget

Creating a Budget

Has the end of the month ever rolled around and you’re scraping pennies out of the couch cushions to pay for a cheap meal?! Do you sometimes look at your bank account and wonder how on Earth you ended up over drafting again? Budgeting your money is not a natural instinct you’re born with! It’s something you have to learn to do and practice over time, so don’t worry if you’ve made mistakes in the past. You can start budgeting today. It just takes a little time to create a budget.

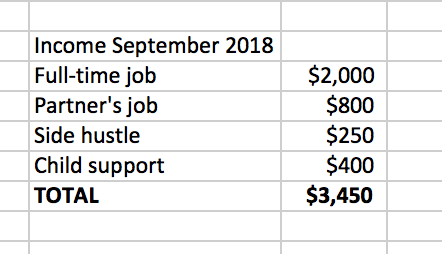

#1 Track Your Total Income

You can’t begin to follow a budget until you are clear as crystal about what money is coming in and what money is going out. So first thing, start by writing down exactly how much money you earn/bring in each month after taxes. If you have a spouse or partner who splits the bills with you, include their income in the budget, too. Remember to include everything from full-time income, side hustle income, alimony/child support checks, social security, pension, disability, or anything else that makes its way into your bank account.

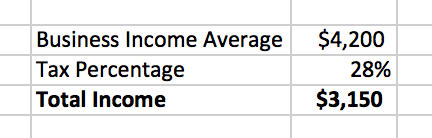

Note: If you are a freelance entrepreneur and your monthly income fluctuates, look at your total income over the past three months and use the average of the three as your income before taxes. Then deduct your taxes to come up with a final income number. If you do not know your tax percentage bracket, speak with your tax specialist or CPA. If you do not have one, you can estimate that 25% of your gross income must be set aside for taxes (although that percentage could be far more or far less, depending on how much money you make).

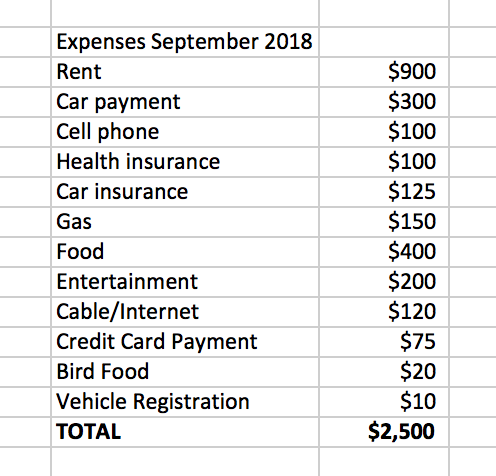

#2 Track Your Expenses

Next, make a list of all of your expenses, including the bills of whomever you included in your income. This is the money you’re spending on a monthly basis. It’s easiest to start by opening up your bank and credit card statements and peeling through one entire month from beginning to end. You’ll want to write down regular bills like mortgage, car payments, cell phone, cable, and credit card payments.

Once you’ve written those down, scan through your statements to find irregular bills that might be invoiced every few months like your HOA, insurance, or vehicle registrations. Finally, come up with an average number for food, entertainment, pet bills, gas, electricity/water, and anything else you regularly spend your money on based on the past three months.

Note: If you regularly spend cash instead of using a debit card, credit card, or check, spend a month logging every purchase you make to get a clear picture of where your money is going. Tracking and logging cash expenditures is far more tedious, but it is possible with some focus. Try an app like EveryDollar to help you!

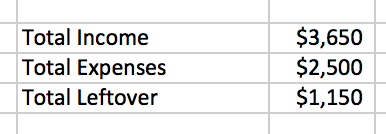

#3 Calculate Your Net Income

Add up your total income after taxes and subtract from it your total estimated expenses. Are you left with a positive number? Great! That means you’re not spending more than you earn! If the number is negative, you’ll need to determine which expenses you can cut to get to that positive number.

#4 Balancing Your Budget

Once you can plainly see, in black and white, how much money you’re spending versus how much money you’re earning, it’s time to set a goal. If you’re currently spending more than you make, your goal should be to balance your budget. That means you’ll need to look at monthly spending and determine which numbers can be lowered. Then, look at your monthly earning and decide whether or not you can make more money than you’re currently making.

This is where budgeting can be difficult! Expenses like food, entertainment, and gas/transportation are all numbers that are truly up to you. Sure, you have to eat, go places, and occasionally experience some entertainment; you can usually lower these numbers if you’re honest about how much you need in each category. Often time cell phone bill can be lowered and your cable bill can be eliminated entirely. Do this until you see that your income number is higher than your expenses number.

#5 Start Saving

If your income is already higher than your expenses, write down the amount of money leftover at the end of each month. Your first goal should be to build a savings account. Having three, or better six, months worth of income in a savings account gives you the comfort of knowing your bills are paid even if something affects your ability to make income for a while. If you have a savings account, your goal might be to pay off a credit card faster or save up for a vacation/special occasion. The money leftover at the end of each month should go towards your financial goal. Once you reach that goal, you get to move on to another one!

#6 Stick to Your Budget

Now that you have a budget, you have to follow it. That means you have to track your money and pay attention for unexpected bills that could affect your goals. Using an app like EveryDollar or Mint everyday will give you a clear view of where your money is going and what you can do to get closer to your goals. Setting these apps up on your phone or computer only takes about 20 minutes, and both apps automatically download new purchases made with your debit or credit cards so that you can categorize them (label them “food” or “rent”, etc.).

#7 Check in Regularly

Checking your finances should be a daily habit. At least once each day you ought to be logging in to see what you’ve spent money on and where you can cut back. The error most people make when creating a budget is having no plan for following up with that budget, and the truth is that you cannot accurately keep yourself on track just by checking in once or twice a week. The good news is, checking in everyday only takes about 3 minutes.

#8 Update Your Budget Every 6 Months

Reassess your budget twice a year as a rule. Even if you don’t think anything has really changed, it’s worth a second look so that unexpected expenses don’t begin to creep up on you. In the first few months, you may find yourself updating and tweaking your budget as you notice more expenses you didn’t log in your first draft. The more accurate a budget you can create, the better. And of course, if your job changes or your rent goes up, you’ll need to update your budget immediately.

Recap

Creating a budget and finding out you’re not making as much as you spend can feel hopeless. But without a budget, you won’t have the information and tools you need to balance your finances and eventually get back on top. Facing reality might be difficult at first, but it’s completely worth it to get clear on your money and make a plan to get to where you want to be.

Disclaimer: Content found on loanreviewhq.com has been created to be used for informational purposes only and help readers achieve a basic understanding of their finances and financial options. The content is not intended to replace or usurp financial advice from professional accountants, CPAs, etc. If you you’re seeking financial advice, always present any questions you may have regarding your finances to a professional. Never disregard professional advice because of something you read on the internet.